A cash flow statement is a financial statement that shows how cash entered and exited a company during an accounting period. Cash coming in and out of a business is referred to as cash flows, and accountants use these statements to record, track, and report these transactions.

In this guide, we’ll go over:

- Cash Flow Statement Definition

- Cash Flow Statement Components

- Example of a Cash Flow Statement

- How to Prepare a Cash Flow Statement

- Cash Flow Statements vs. Other Financial Statements

- Showing You Understand Cash Flow Statements on Resumes

Cash Flow Statement Definition

A cash flow statement may go by a few different names — CSF, statement of cash flow, SCF, or consolidated statement of cash flows — but each name represents the same thing: a financial statement where a company’s operating, investing, and financing activities are reported in terms of incoming and outgoing money.

Cash moves into and out of a business for various reasons, sometimes unrelated to the direct sale of products, goods, or services. The cash on these financial statements includes current assets, like money in checking and savings accounts, and cash equivalents, like short-term investments.

Cash flow statements explain how the company manages this cash. For example, a CSF can show if a company is taking on excess financing to fund operations but isn’t generating enough cash to support those debts.

Who Uses Cash Flow Statements?

Creating financial statements is a core responsibility of accountants and a company’s finance team. These finance professionals also utilize cash flow statements and other financial reports to analyze and evaluate a business’s performance. In budgeting, finance teams can look at cash flows from previous accounting periods (e.g., month, quarter, year) to see where they should make spending adjustments. In business strategy, these financial statements can illuminate where a company is overspending and inform changes to the company’s overall approach.

Additionally, certain areas of corporate finance, like investment banking, private equity, and mergers and acquisitions (M&A), rely on these statements as a core part of analyzing and predicting a company’s financial standing. For example, an investment banking analyst may use a company’s cash flow statement when calculating a discounted cash flow (DCF) valuation. Learn how this works in the real world with Bank of America’s Investment Banking Virtual Experience Program.

Cash Flow Statement Components

A statement of cash flows displays incoming and outgoing money from three types of activities: operating, investing, and financing.

Operating Activities

Cash flows from operating activities include money spent or generated by selling products, goods, or services. Line items in this section may include:

- Depreciation and amortization: how much an asset loses value over the course of its lifetime

- Changes in working capital: transactions that affect current assets or liabilities

- Accounts receivable: money owed to the company by clients and customers

- Accounts payable: money the company owes to clients and customers

- Inventory: sellable products or goods

Investing Activities

Investing activities include changes to long-term assets, such as real estate, and changes in capital expenditures (CapEx). Line items for this section include:

- PP&E purchases: plant, property, and equipment (PP&E) purchases, such as warehouse space, office equipment, or production plants

- Proceeds from PP&E sales: money generated from selling PP&E

- Purchase of marketable securities: buying stocks or bonds

- Proceeds from sale of marketable securities: money generated from selling stocks or bonds

- Business acquisition proceeds: money made or spent as part of acquiring another business or part of the company being acquired

Financing Activities

Cash flows from financing activities involve any money spent or generated from issuing debt, paying dividends to shareholders, and repaying long-term loans. Line items in the financing activities section include:

- Dividend payments: Revenue or earnings redistributed to shareholders as cash or stock reinvestments

- Repurchase of common stock: Buying back previously issued public shares

- Proceeds from issuing debt: Money made by selling debt to investors

- Repayments of long-term debt: Money spent to repay loans

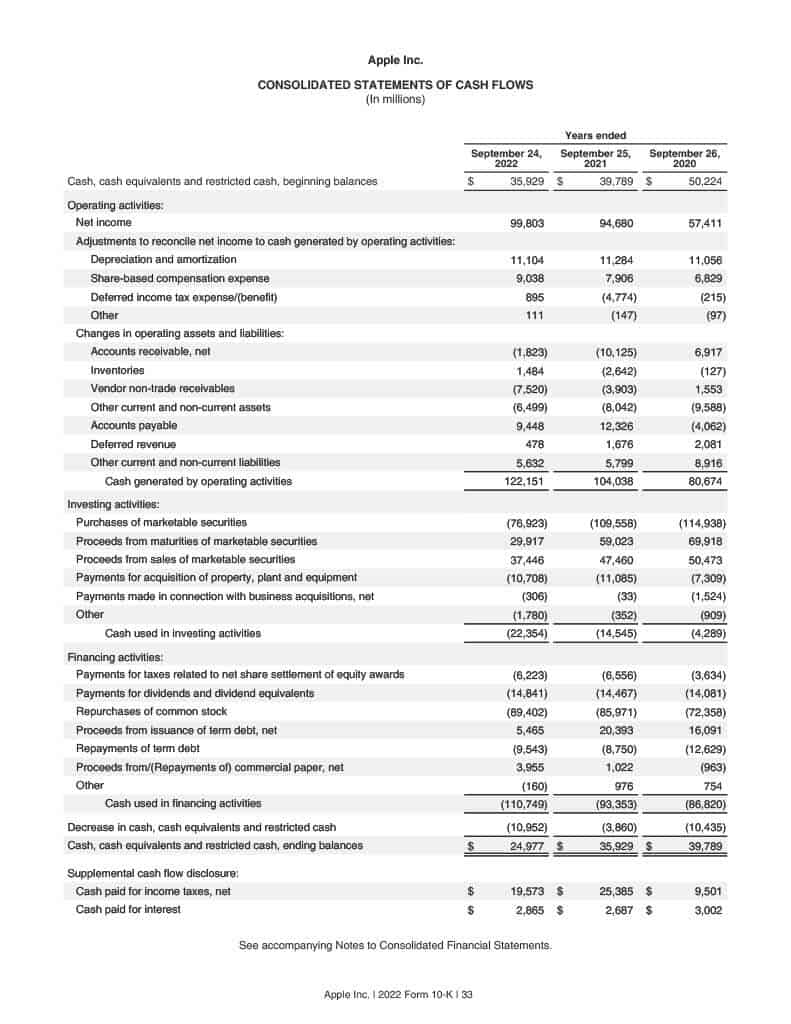

Example of a Cash Flow Statement

Using Apple’s annual financial report for the fiscal year 2022, we can see an example of what cash flow statements look like for a large corporation.

How to Read Cash Flow Statements

The most important thing to remember when reading a cash flow statement is that numbers in parentheses are negative flows of cash or money spent. Conversely, numbers without parentheses are inflows of cash or money received.

Financial statements typically compare balances to previous accounting periods. For example, a monthly cash flow statement may also feature balances from the previous month or the same month in the previous year.

Generally speaking, if the overall cash flows for the accounting period are positive, a company is generating cash in a healthy manner. However, that doesn’t mean that a company with negative cash flow totals is necessarily unhealthy. For example, negative cash flows can be due to a strategic growth plan or because the company is relatively young and is still finding its way to profitability.

How to Prepare a Cash Flow Statement

Creating a cash flow statement is a four-step process:

1. Calculate Operating Activities Cash Flows

Accountants have two methods to choose from when calculating operating cash flows: direct or indirect cash flows.

Direct Method

The direct cash flows approach involves adding all the cash the company made or paid for the reporting period. This includes money paid to suppliers, salary payments, and cash from selling products or services. Businesses that use the cash basis of accounting typically use the direct method. In cash basis accounting, money is only counted when it is actually received or spent by the business. The opposite of this is the accrual basis of accounting which counts cash if earned or expensed, even if those transactions have not been completely processed.

Indirect Method

The indirect cash flows approach involves using the company’s net income and adjusting it based on non-cash transactions. For example, if the balance of accounts receivable increases, that increase is revenue but not cash because the money has not been received yet.

Some accounts must be added to net income for an accurate CFS. For instance, depreciation and amortization are subtracted from revenue to get net income. These are not cash transactions, though, even if they affect the company’s overall profits. Cash flows are only explicit additions or subtractions to the company’s cash balances.

Choosing Which Method to Use

Although the indirect cash flow approach may seem more complicated, it is the most commonly used approach. This is because accountants can easily find most of the adjustments to net income on the company’s balance sheet. On the other hand, the direct method is more time-consuming and has higher chances of error if a receipt is missing or transactions are inaccurate.

2. Calculate Investing Cash Flows

Calculating investing cash flows involves tallying up any cash spent or generated from buying property, selling real estate, investing in office equipment, or acquiring a business. These cash flows only include transactions completed with free cash or money the company has on hand to spend. Investing cash flows do not include transactions that use financing or debt.

3. Calculate Cash Flows from Financing Activities

When calculating financing cash flows, accountants should include debt and equity financing — money used to fund the business and pay back borrowed funds. U.S.-based accountants who adhere to generally accepted accounting principles (GAAP) should list shareholder dividends in the financing activities section. However, international accountants who follow international financial reporting standards (IFRS) should include dividends as part of operating activities instead.

4. Calculate Ending Balance

Each section of the cash flow statement should have a total balance — total cash flows for operating activities, investing, and financing. At the end of the statement, these totals are combined to determine the company’s total cash flow balance for the period. A positive cash flow means the company had more cash coming in than it spent. On the other hand, a negative balance suggests the company spent more than it generated.

Cash Flow Statements vs. Other Financial Statements

A statement of cash flows is one of the core financial statements used to understand a company’s economic performance and health. The other two statements used are:

- Balance sheets: A balance sheet details a company’s assets for the reporting period and explains how those assets are financed by equity, debt, or a mix of the two.

- Income statements: An income statement shows where a company’s revenue comes from and explains how gross revenue is adjusted to net profits.

The CFS bridges the income statement and balance sheet by showing how a company’s assets and liabilities translate into revenue-affecting transactions. Cash flow statements can also give a more accurate look at the company’s available cash. For example, an income statement shows revenue and expenses. However, some of those expenses may not have actually been paid yet, and some revenue may not have been collected at the time of reporting. Statements of cash flows show the actual accrued and spent cash for the reporting period.

Find your career fit

Discover if this is the right career path for you with a free job simulation.

Showing You Understand Cash Flow Statements on Resumes

You can demonstrate an understanding of how to use cash flow statements by mentioning specific formulas, business valuation methods, and financial metrics that rely on these statements.

Some formulas or metrics you can mention are:

- Discounted cash flow (DCF) valuation

- Calculating net present value (NPV)

- Calculating free cash flows

- Calculating net cash flows

If your work or internship experience included creating financial statements, include that in the description of the job or internship. For example, mention if you had an internship where you prepared a business’s income sheets, balance sheets, and cash flow statements. You can also add “creation of financial statements” to your resume’s skill section.

Hone your skills with Forage’s finance virtual experience programs.

Image credit: AndreyPopov / Depositphotos.com